Investment Process

The heart of our investment process is based on in-depth and continuously updated proprietary research combined with the experience and insight from investing in emerging markets.

We seek a high degree of conviction in our investments by achieving a deep level of understanding of the companies and countries in which we invest and by applying private equity style investment techniques when investing in listed companies.

Implementing the correct investment timing is a significant source of superior returns in emerging markets, where price movements are more volatile than in developed economies. Our investment process is therefore designed to act nimbly whilst retaining a high degree of confidence. With members of the research team frequently visiting companies, we hold intra-week investment committee calls as required to ensure market timing is optimized.

We employ a series of filters so as to identify investments for our funds: at the macro, company specific and at the trigger/catalyst level, making use of timing to identify entry and exit points in both long and short positions.

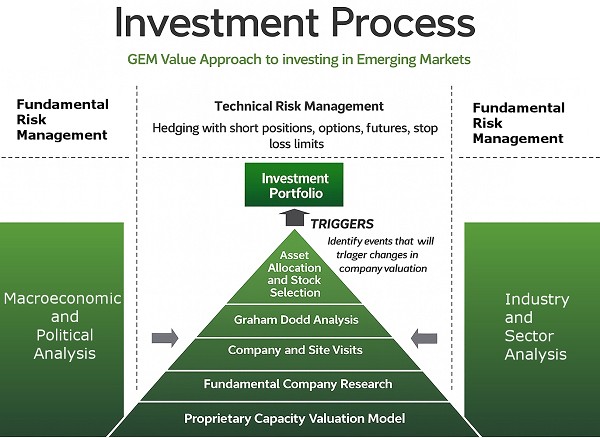

Our investment process is therefore three-fold:

- A combination of bottom-up and top-down in-depth analysis

- The identification of key catalysts and triggers that will drive valuations

- Timing

IN-DEPTH RESEARCH

In-depth research is crucial to all of our investment decisions. By going the extra step in our research, we seek to identify deep value at the beginning of the return curve.

By meeting on a regular basis with investee companies and their competitors, as we!l as sector contacts, we achieve a very deep understanding of the factors driving the companies as well as the sectors in which they operate. This approach allows us to identify incorrect valuation and opportunities, as well as likely triggers and catalysts which have already occurred in other countries or companies and may have a knock-on effect.

BOTTOM UP

On the bottom-up side, we place a special emphasis on identifying catalysts and triggers within companies. These can include potential management changes or liquidity issues that could lead to a share price revaluation. We then conduct probability analyses of the likelihood of these catalysts and triggers occurring and how they may each impact on a company’s performance. In total, we cover approximately 750 companies worldwide.

In addition to financial modelling, we go one step further and analyse companies from a potential acquirer’s as well as a competitor’s point of view. The former allows us to identify M&A and consolidation opportunities; the latter allows us to identify sector trends, opportunities, operational issues and total sector capacity. By developing long-term forecasts, we increase our conviction rate and feed this into our investment allocation process.

Meeting with company management is fundamental to us: we meet with companies, at both board and operational management level, as well as their competitors, on a regular basis. We will also hold a refresher meeting with a company just before we invest if we have not recently met with them. Accessing company information in some emerging market countries can be difficult, sometimes requiring face to face meetings. We always use direct source data in our models and will never compromise on this, preferring to postpone or not to invest if that is the case.

TOP DOWN

When considering an investment into a company, the first filter is at the macro level. We examine the macro picture of the country and the region of each potential investment, including interest rate variables and trends, political factors, inflation, GDP, earnings growth, currency movements and trading partners. We contrast this with other emerging and world markets, assessing the implied and relative valuations of markets for equities, bonds, cash, property and commodities.

We pay special attention to country- and sector-specific triggers and catalysts that will drive valuations. These can include impending regulatory changes which will affect the sector, supply/demand imbalances, industrial restructuring themes and sector consolidation.

Furthermore, we wiII only invest in a particular country once it fulfils certain top-down criteria.

TRIGGERS & TIMELINESS

Determining the triggers and catalysts at a country, sector and company level is a critical factor in our successful investments. In emerging market economies, the pace of change is usually much faster than in developed economies and may catch many investors unaware . We seek to capture a larger share of value by being able to interpret these triggers and catalysts quickly and accurately.

Timeliness is crucial to our investment proposition. As soon as we begin to identify a catalyst or trigger, we will research it in depth . This allows us to react much more quickly in making investment decisions and to capture a larger portion of the upside, whilst stili maintaining a high degree of confidence

RİSK MANAGEMENT

The company's risk management is mainly company specific. As value investors, we seek to minimize risk by having an in-depth understanding of the companies in which we invest and by carefully assessing the risks associated with each company. Prior to investing in a company, we will apply a top down, macro filter to the countries in which investments are located, as well as assessing the countries that may impact on them.

The company's knowledge of each market, from both a macro and a company specific perspective, enables us to act quickly during market downturns.

All funds and client portfolios are also reviewed on a monthly basis in order to prepare monthly reports for distribution to clients. General conditions in the economy and financial markets are continuously monitored as are changes in monetary and fiscal policy, inflation, supply and demand, geo-political and social factors. Factors triggering investment reviews, and perhaps also triggering investment recommendations, include changed general conditions in government stability, the economy and all markets including currency, stock and bond markets.

The emerging market funds which invest worldwide have a majority of their assets in highly liquid positions, with one-two day liquidity. Smaller positions in other funds may have a liquidity of between three to ten business days, which is the general norm for smaller emerging market companies.